How Policy Certainty Powered the Rise of U.S. Solar Module Manufacturing — and Why That Growth Is Now at Risk

- Jul 21, 2025

- 4 min read

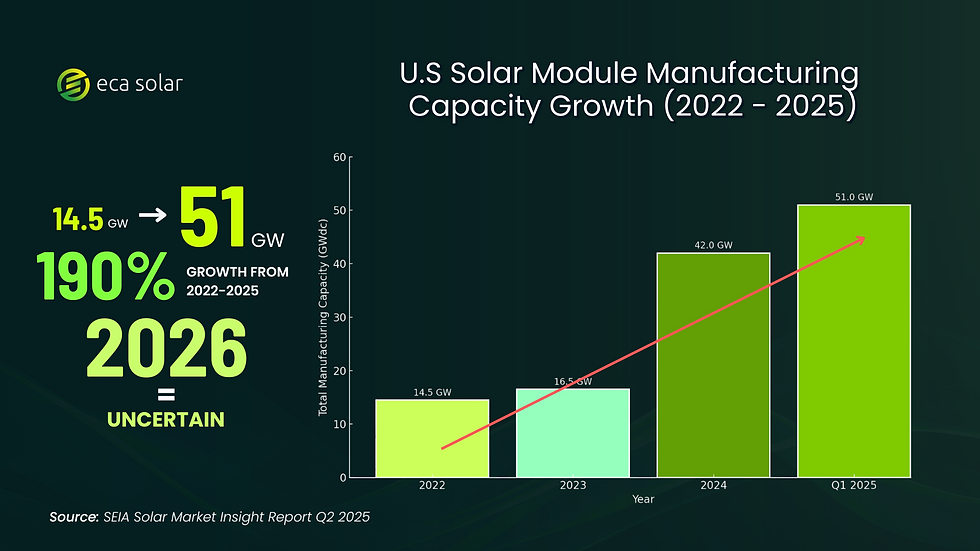

Between 2022 and the beginning of 2025, U.S. solar module manufacturing capacity jumped from 14.5 GW to over 51 GW — a staggering 190% increase in just over two years. This rapid expansion wasn’t coincidental. It was driven by a stable and ambitious federal policy landscape, particularly the passage of the Inflation Reduction Act (IRA) in 2022. But now, that momentum is under threat.

The Role of Policy Certainty in U.S Module Manufacturing

The Inflation Reduction Act (IRA) created an environment where long-term planning for solar development finally made sense. Solar developers and module manufacturers alike responded to the market signals it sent. By offering a decade-long extension of the Investment Tax Credit (ITC) and Production Tax Credit (PTC), plus generous bonus credits for domestic content, energy communities, and low-income service areas, the legislation allowed companies to confidently invest in U.S.-based manufacturing.

The law also introduced new manufacturing tax credits (45X and 48C) that directly incentivized the production of solar components on American soil. This is what laid the foundation for the surge in domestic module production we’ve seen over the last two years. It wasn’t just about installing solar panels — it was about building the supply chain to support them. As a result, more than a dozen new module manufacturing facilities were announced or came online in 2023 and 2024. These included major investments like First Solar’s new $1.1 billion plant in Alabama and Qcells’ $2.5 billion expansion in Georgia — two of the largest solar manufacturing investments in U.S. history. According to SEIA, this buildout raised capacity from a modest 16.5 GW in 2023 to 42.2 GW by the end of 2024, and further to 51.1 GW in early 2025.

Why the Growth is Now at Risk Under the OBBBA

The recently passed One Big Beautiful Bill Act (OBBBA), signed into law in July 2025, alters this trajectory. Though positioned as a budget reconciliation measure, it includes sweeping changes that roll back many of the IRA’s clean energy provisions. For a deeper dive into the legislation and how it impacts solar developers, read our breakdown here. Among the most concerning for solar developers and manufacturers:

Sunsetting of Tax Credits: Under the OBBBA, solar projects must begin construction by June 30, 2026, and be placed into service by December 31, 2027, to qualify for the full ITC or PTC. After that, the credits fall sharply and disappear entirely. This removes the decade-long runway the IRA provided.

Restrictions on Safe Harboring: The OBBA narrows the ability to "safe harbor" by requiring that physical construction, not just financial commitments, begin physical construction by June 30, 2026 to qualify for tax credits. This change eliminates the flexibility developers once had under the IRA, raising risk and reducing confidence in multi-year project planning.

Foreign Entity of Concern (FEOC) Compliance: Beginning in 2026, projects that use components or receive material assistance from “specified foreign entities” — including companies with substantial ownership or influence from certain foreign governments — will no longer be eligible for the 48E/45Y tax credits. While this policy is aimed at strengthening national security and promoting domestic sourcing, it introduces substantial supply chain complexity.

Though the policy may seem to support U.S. manufacturing, the opposite is likely to occur. The current domestic supply of FEOC-compliant materials remains limited. Without sufficient time to scale production and diversify sourcing, developers may face project delays or cancelations due to noncompliance risks. In turn, this suppresses demand for U.S.-made solar modules — undermining the very manufacturing growth the policy intends to encourage.

With shorter timelines, less flexibility, and stricter sourcing rules, the stable policy environment that enabled U.S. solar’s 190% growth has been replaced by a wave of uncertainty — threatening both project development and future manufacturing investment.

What It Means for the Industry

At ECA Solar, we believe this moment is pivotal. The 190% growth we've experienced is proof of what’s possible when federal policy aligns with private sector ambition. But the rollback of these incentives threatens to stall further expansion just as the industry gains traction.

Manufacturers are now reconsidering expansion plans and solar developers are questioning the viability of late-stage projects. And investors are reevaluating risk amid tighter deadlines and fewer guarantees. If the U.S. is serious about solar leadership, it must now focus on adapting to these new policies with long-term strategies that preserve momentum and protect the gains already made.

The Bottom Line

Our latest infographic charts the explosive growth in U.S. solar module manufacturing from 2022 to 2025. But what it doesn’t show is the uncertainty ahead. Without a stable policy framework, the gains made in recent years could evaporate.

Now is the time for policymakers to recommit to long-term solar support. The future of our energy transition — and the jobs and investments tied to it — depend on it.

Great post! The Inflation Reduction Act clearly boosted U.S. solar manufacturing, showing how policy certainty drives growth. Building strong supply chains is key, and as a freight agent in Karachi, I’ve seen how efficient logistics make a big difference in large energy projects.